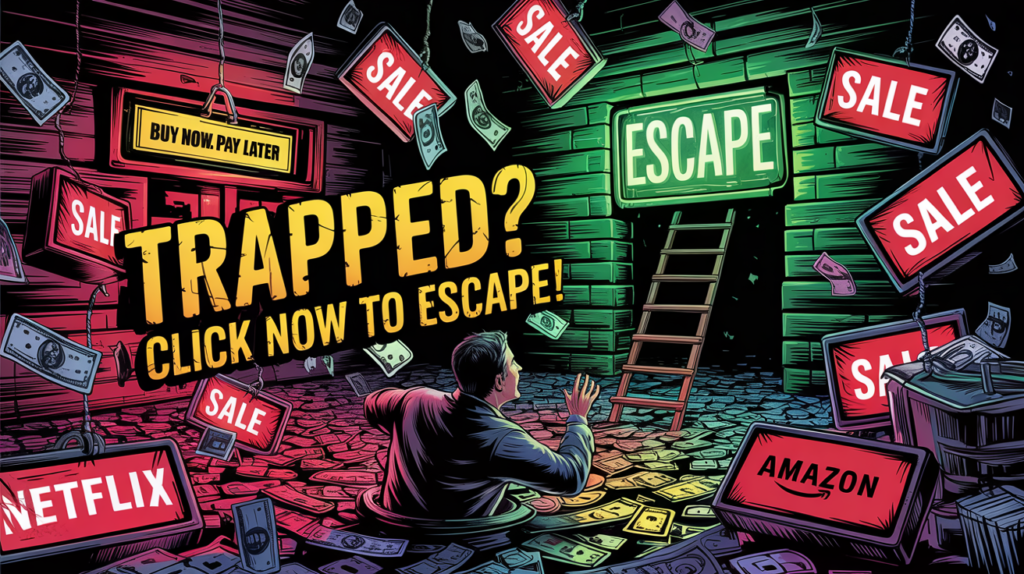

Your bank account is bleeding, and you might not even realize it. Every day, sneaky financial traps are draining your hard-earned cash—disguised as harmless habits, “great deals,” or even “necessities.” The worst part? You’re not alone. Millions are stumbling into these money pits, and the longer you stay trapped, the harder it is to climb out. But don’t panic yet—there’s a way out, and this article is your lifeline. Let’s expose these hidden money traps and arm you with practical, no-nonsense strategies to escape them right now.

Trap #1: Subscription Creep – The Silent Budget Killer

You may also like

You signed up for that streaming service for one show. Then came the fitness app you swore you’d use, the premium cloud storage, and that “just $5 a month” newsletter. Sound familiar? Subscription creep is the modern-day money trap you don’t see until it’s too late. A recent study found the average person spends over $200 a month on subscriptions—many of which they don’t even use.

Why It’s Dangerous: These small charges seem insignificant, but they stack up fast. Before you know it, you’re shelling out hundreds a year on stuff you barely touch.

How to Escape: Audit your subscriptions today. Check your bank statements for recurring charges, cancel anything you haven’t used in 30 days, and ask yourself: “Do I really need this?” Pro tip: Use a free app like Rocket Money or Truebill to track and kill off the leeches automatically.

Trap #2: The “Buy Now, Pay Later” Scam You’re Falling For

That new couch or shiny gadget looks tempting when it’s split into “four easy payments.” But here’s the dirty secret: Buy Now, Pay Later (BNPL) schemes are a wolf in sheep’s clothing. Sure, they promise no interest—but miss a payment, and the fees hit like a freight train. Worse, they trick your brain into overspending because it doesn’t feel like real money.

Why It’s Dangerous: BNPL users are 68% more likely to rack up debt, according to financial experts. It’s a slippery slope to living beyond your means.

How to Escape: Stop treating BNPL like free money. If you can’t afford it upfront, you can’t afford it—period. Save up instead, or hunt for secondhand deals on platforms like eBay or Facebook Marketplace. Your wallet will thank you.

Trap #3: Lifestyle Inflation – The Trap That Keeps You Broke

Got a raise? Nice! New car, bigger apartment, fancier dinners—uh-oh. Lifestyle inflation is the trap where every extra dollar you earn gets swallowed by “upgrades” you don’t need. You’re working harder but somehow still scraping by.

You may also like

Why It’s Dangerous: It locks you into a cycle of needing more money just to maintain the life you’ve built. Retirement? Savings? Forget it—you’re too busy keeping up appearances.

How to Escape: Freeze your lifestyle now. When extra cash comes in, funnel at least 50% into savings or debt repayment before you’re tempted to splurge. Automate it with a high-yield savings account (think 4%+ interest) and watch your safety net grow instead of your expenses.

Trap #4: The Convenience Tax You’re Paying Without Knowing

Grabbing takeout because you’re too tired to cook? Ordering groceries online with a $10 delivery fee? That daily $5 latte? These “conveniences” come with a steep hidden tax that’s eating your budget alive. A quick calculation: $5 a day on coffee alone is $1,825 a year. Yikes.

Why It’s Dangerous: It’s death by a thousand cuts. Small, impulsive spending feels justified in the moment but leaves you wondering where all your money went.

How to Escape: Plan ahead. Meal prep once a week to dodge takeout temptation—start with simple recipes like overnight oats or sheet-pan dinners. Brew coffee at home (a $20 coffee maker pays for itself in a week). And unless you’re bedridden, skip the delivery fees and shop in person. Convenience is a luxury you can’t afford to overpay for.

Trap #5: Falling for Fake Discounts and Flash Sales

“50% OFF – TODAY ONLY!” screams the ad. Your heart races, your mouse hovers over “Add to Cart.” But here’s the kicker: Most “sales” are engineered to make you spend more, not save. Retailers jack up prices before slashing them, or push you to buy junk you’d never want otherwise.

Why It’s Dangerous: You’re not saving money—you’re just spending it faster. Impulse buys during sales account for billions in wasted consumer dollars annually.

How to Escape: Pause and breathe. Before buying, ask: “Would I want this at full price?” If the answer’s no, walk away. Use price-tracking tools like Honey or CamelCamelCamel to see if it’s really a deal. Better yet, unsubscribe from those sale emails clogging your inbox—they’re bait, not blessings.

Trap #6: The “I’ll Save Later” Delusion

You tell yourself you’ll start saving when you’re “more stable”—after the next paycheck, the next raise, the next whatever. Spoiler alert: “Later” never comes. Meanwhile, compound interest—the magic that could’ve turned $100 into $1,000 over decades—is slipping through your fingers.

Why It’s Dangerous: Time is your biggest asset, and delaying savings robs you of it. Waiting just five years to start investing can cut your retirement nest egg in half.

How to Escape: Start small, start now. Even $20 a month in a low-cost index fund (like Vanguard’s VTI) can snowball over time. Set up automatic transfers so you don’t have to think about it. Future you is begging for this.

You may also like

The Wake-Up Call You Can’t Ignore

These traps aren’t accidents—they’re designed to keep you broke, stressed, and stuck. But here’s the good news: You’re not powerless. Every dollar you reclaim from these money pits is a step toward freedom—freedom from debt, from paycheck-to-paycheck living, from the nagging fear you’ll never get ahead.

Take action today. Audit your subscriptions, ditch the BNPL habit, freeze your lifestyle, cut the convenience tax, ignore fake sales, and start saving. It’s not sexy, but it’s real—and it works. Your bank account isn’t doomed yet, but the clock’s ticking. Escape these traps now, or risk regretting it forever.